Top Runner 2026

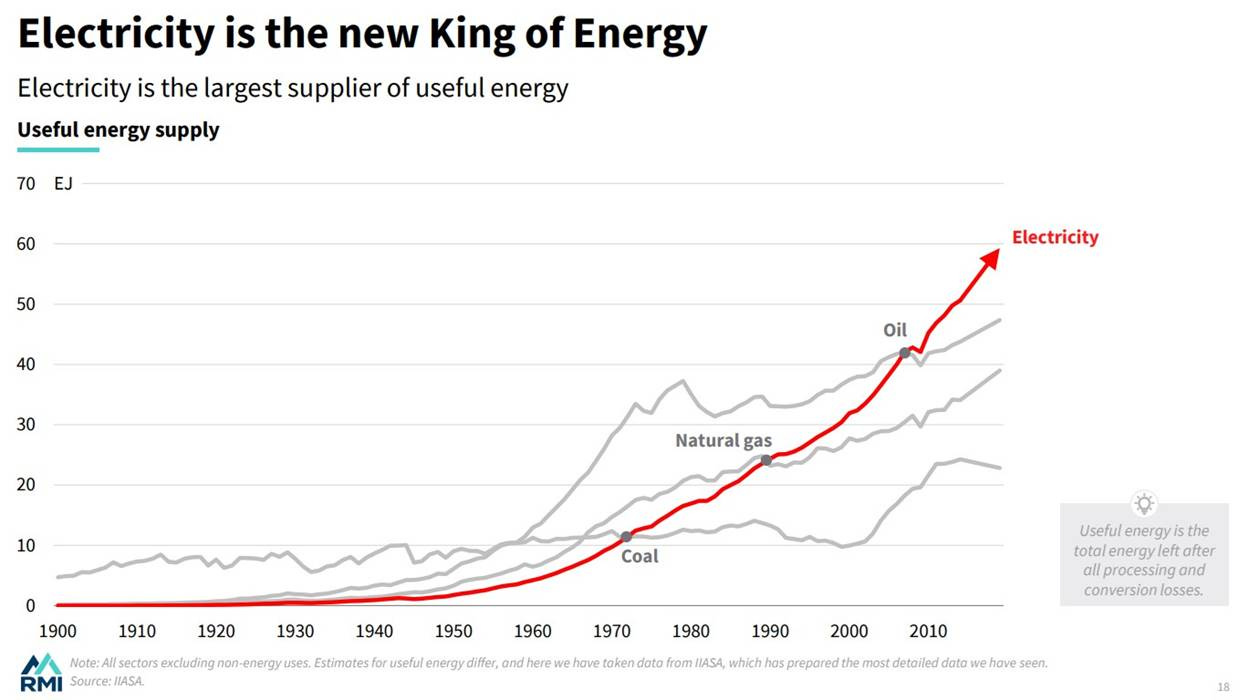

Electricity’s Triumph in Japan

In this post I am going to explore an investment idea in Japan related to the growth in electricity and semiconductor industries. But before I do that I want to highlight a Substack article Noah Smith wrote in 2024 titled:

“The triump of electormagnetisim over thermodynamics”

I think this post by Noah highlights one of the longest-term trends in investing today and is a must read. Here are excerpts from the article:

“We all laughed, but the joke was deeply rooted in technological reality. To this day, most power sources — including nuclear power — basically just heat up water, which turns it into steam, which pushes some sort of a wheel, which either A) turns some gears that make a machine run, or B) turns a magnet that generates an electrical current. For fossil fuel power sources (although not for nuclear), this involves combustion — the rapid release of heat from chemical reactions.

Combustion is one of humanity’s two main methods for extracting and transporting energy. Understanding how to harness combustion was probably the most important technological revolution in human history. The energy provided by coal-powered steam engines, and then by oil-powered internal combustion engines, was what allowed the creation of mechanized agriculture, modern manufacturing, rail transport, cars, trucks, modern shipping, powered flight, and most of the things that raised humanity up out of the muck of abject poverty where we started.

But a second technological revolution was underway at the same time, which also changed the face of our world. This was electricity — the ability to move electrons through conducting materials.

Electricity and combustion are complementary — for example, when you burn coal to boil water to turn a turbine to turn a generator that creates electricity. And of course both rely on some form of chemical potential energy — a gas tank, a battery, etc. —to transport stored energy from place to place.

But ultimately these are two very different ways of moving energy around. Combustion happens in a disorderly rush, as rapid chemical reactions release heat in an uncontrolled fashion. Electricity is a far more stately and controlled process, pushing electrons deliberately through wires and other conducting materials. To understand combustion, you need to understand the physics of random motion; to understand electricity, you need the more precise physics of how electromagnetic fields move charged particles around. The two people pictured at the top of this post, James Clerk Maxwell and Rudolf Clausius — worked out some of the key theories of electrodynamics and thermodynamics, respectively.1 Those were two of the greatest and most important intellectual triumphs in human history.

through application of thermodynamics. I HOPE THAT CLEARS THINGS UP")

… Eventually, though, as the economist Paul David has documented, manufacturers figured out how to use electricity’s precision to do things they could never do with combustion alone. They could bring power to a bunch of small independent workstations instead of having everyone working on one giant assembly line. This let them use power only when needed, and only in precise amounts. It also gave production engineers much more flexibility in rearranging factories to optimize production processes. The result was a tremendous, long-lasting boom in manufacturing.

Another little dust-up between combustion and electricity was in the automotive space. A lot of people tried to make and sell battery-powered cars in the early part of the 20th century. Ultimately, the greater power of internal combustion engines, and the high energy density of gasoline and diesel, doomed EVs for a century.

So anyway, electricity and combustion coexisted for a century. But then a few things changed, which significantly increased electricity’s advantages and shored up its weaknesses.

First, a new technological revolution entered the scene — semiconductors. Semiconductors allow us to generate electric power without combustion or other heat-based methods, because they allow us to capture energy directly from solar radiation. Blowing things up and burning things and boiling things, with all the attendant wastage of energy via the randomness of heat, is no longer a necessary step in the process. You can just go straight from natural energy sources to electric currents.

Semiconductors also allowed electricity to improve on its key strengths. It allowed the creation of computers, which can take much greater advantage of electricity’s amazing precision. Computerization allows electric power to be used in an even more targeted and efficient manner than before. A key example is the creation of MEMS (also a semiconductor technology), which allows precision control of drones via software.

Another key example is the brushless electric motor, which uses circuitry to control the currents in an electric motor through electromagnetic fields instead of mechanical devices. Brushless motors are much more efficient, powerful, durable, and easier to maintain than older motors. In any case, there are many more examples besides these two.

I think people still don’t appreciate what a world-changing event this is. The number of basic physical processes that can be harnessed in our Universe is very small. Other than electricity and combustion, humanity really has very few tricks for manipulating the physical world. So when one of these basic control methods suddenly gets much, much better, to the degree where it starts to displace the other, it’s a big deal. It reaches into almost all the major topics I’ve been writing about over the last few years — the Abundance Agenda, competition with China, industrial policy, and so on.

Obviously the biggest effect is going to be an age of abundance. The stagnation of combustion meant a stagnation in energy use and (probably) in productivity as a whole. But electrical technology did not stagnate, and now electricity has finally caught up to the point where it can just replace combustion in a whole lot of physical technologies, and potentially accelerate productivity growth again.”

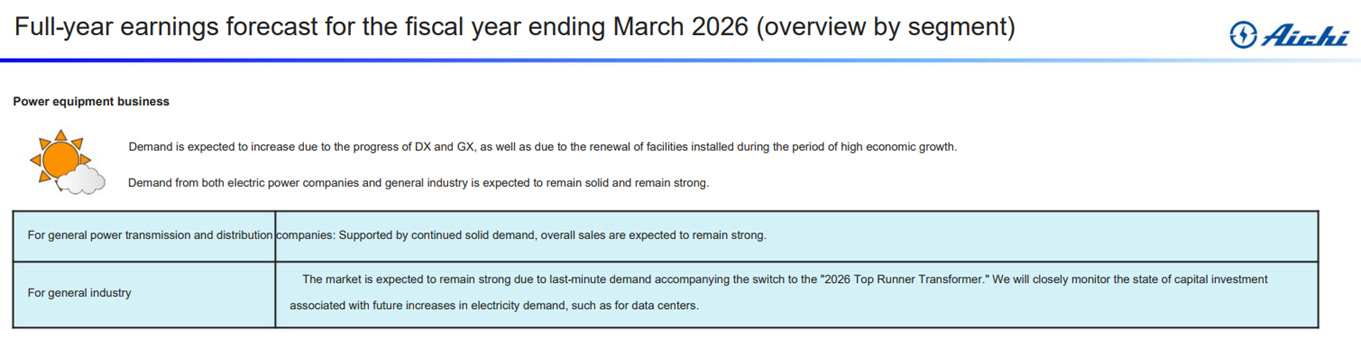

Japan’s Top Runner Program

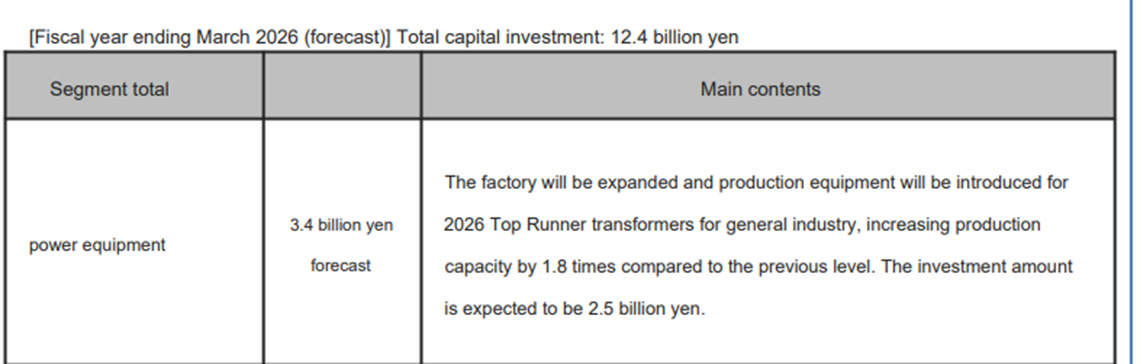

The Top Runner Program is Japan’s flagship framework for energy-efficiency regulation. The he program sets performance targets based on the most efficient products currently available in the market, then raises the benchmark for the entire industry. The upcoming “Third Judgment Criteria,” which comes into effect in 2026, applies stricter requirements to distribution transformers to reduce energy losses, improve power stability, and contribute to Japan’s decarbonization goals.

Aichi Electric (Nagoya: 6623)

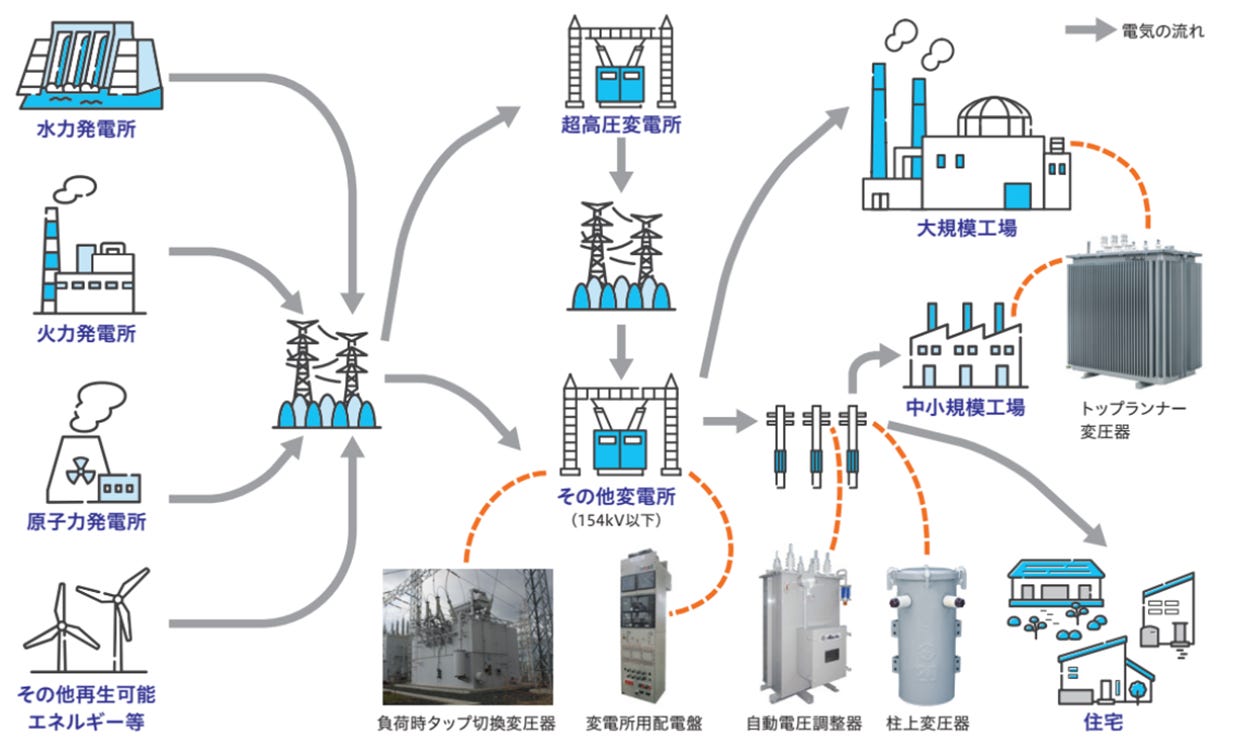

Aichi Electric Co., Ltd. (based in Kasugai, Japan) organizes its operations into three core business divisions. While the company is perhaps most famous for its high-market-share “pole-mounted transformers” seen on utility poles across Japan, its portfolio extends significantly into motor technology and electronics.

The following are the three divisions as typically categorized in their financial reporting:

1. Electric Power Equipment Division

This is the company’s largest and most foundational segment. It focuses on the infrastructure required to transmit and distribute electricity.

Key Products: Pole-mounted transformers (a flagship product), power transformers for substations, and switchgear.

Services: This division also includes the Electric Power System and Industrial System sub-sectors, which handle the construction and maintenance of power plants and electrical substations.

Market Position: They are a primary supplier to major Japanese electric utility companies, maintaining a dominant market share in the distribution transformer market.

Aichi’s core product is transformers and demand has been increasing as Japan’ updates its grid and prepares for higher efficiency standards. Power systems spiked in 2025 as Aichi rebuilt a power plant in the Ukraine that year. This was its first pilot project for overseas sales and it went well.

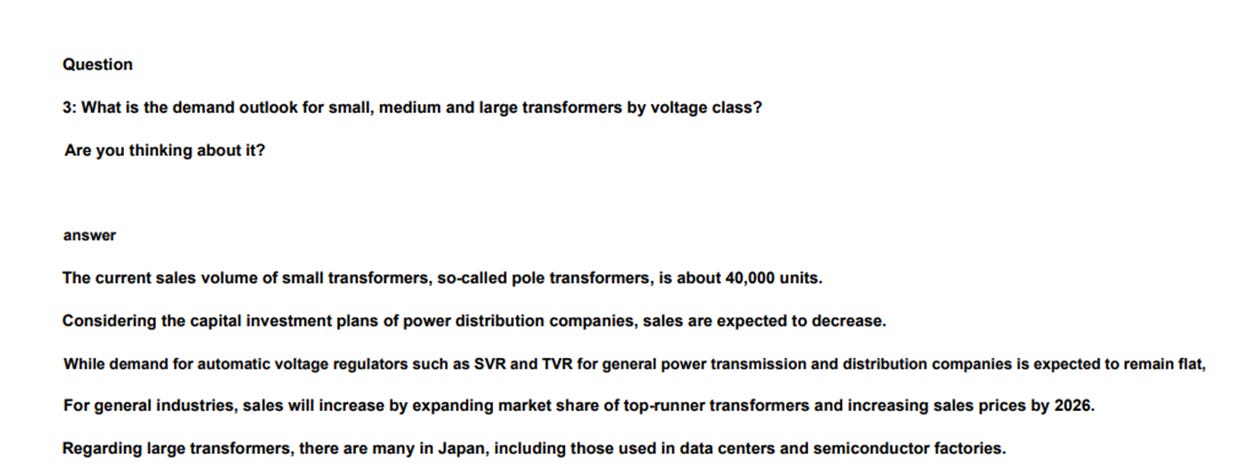

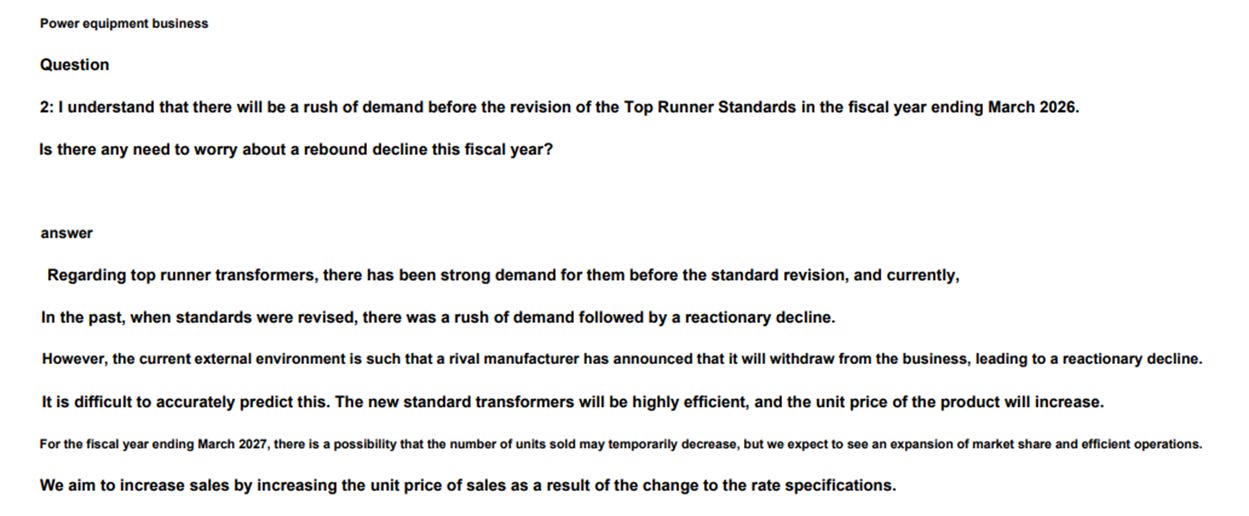

There is a worry that sales will fall due a temporary increase in demand as utilities upgrade ahead of the Top Runner deadline. However, Japan is currently facing a transformer shortage driven by the green transformation, data center expansion, new semiconductor manufacturing plants and the need for grid modernization. With one major manufacturer stepping back to restructure, Aichi Electric has an opportunity to capture “overflow” demand and expand its relationship with utilities.

Top Runner transformer capacity is increasing by 1.8x compared to the previous level in 2026. Now Top Runner transformers aren’t all of transformer sales but it is likely their most profitable. And this line is more automated than the previous transformer manufacturing process so we should expect margins to increase also.

While there maybe yearly fluctuations in sales for different categories of transformers it appears there is increasing long-term demand and Aichi is taking advantage of a competitor exiting the market (likely Mitsubishi Electric which was sold to Hitachi and then Hitachi shut down the transformer segment that competes with Aichi’s Top Runner transformers).

A big risk here in addition to demand declining is rising copper prices and their ability to pass on increases if copper prices do indeed increase.

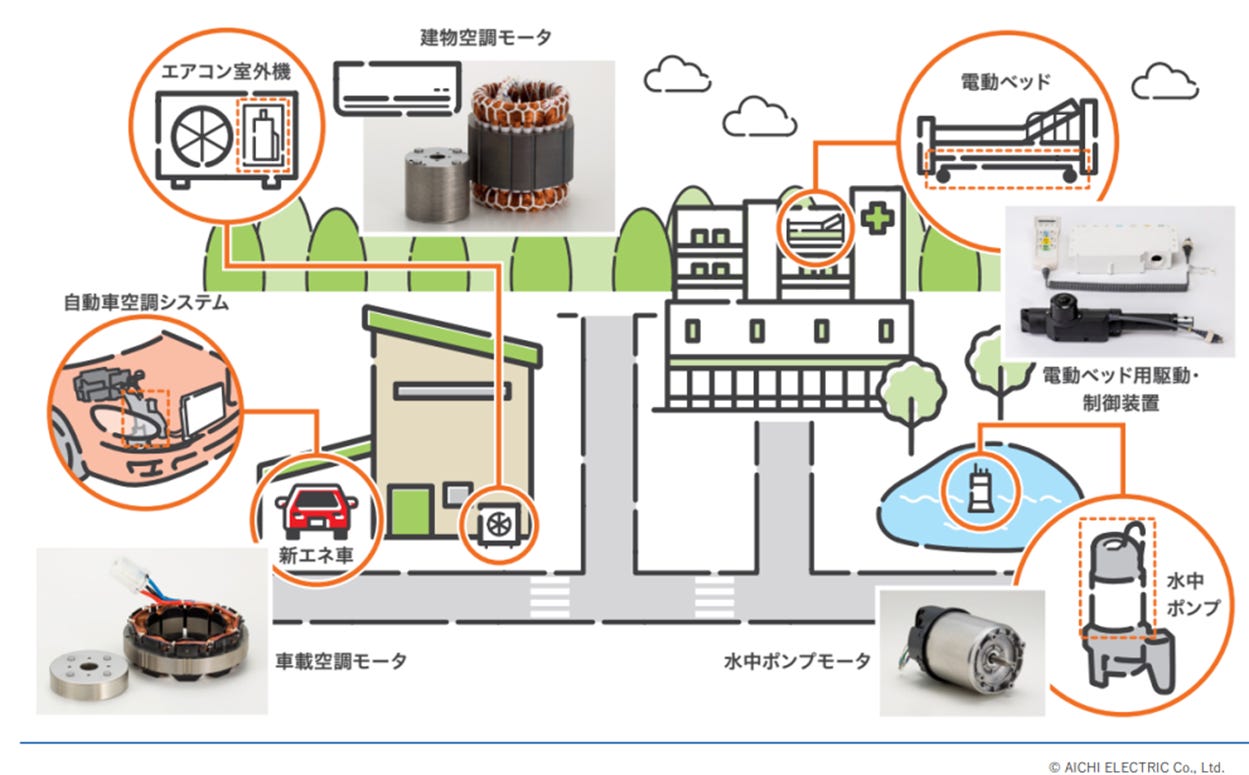

2. Rotary Machine (Motor) Division

This division leverages the company’s expertise in electromagnetics to produce motors and motor-driven appliances for both industrial and consumer use.

Key Products: Small AC motors, brushless DC motors, and hermetic motors (used in compressors).

Applications: Their motors are found in building air conditioning systems, automotive components, and specialized industrial equipment like “shutter operators” and actuators for medical beds.

Innovation: Recently, this segment has focused on high-efficiency motors to align with global energy-saving trends.

This is the least exciting part of Aichi’s business and has faced headwinds from the weakness in the Chinese EV market. But if we exclude Suzhou Electric Motors from this segment we see that the segment’s Japanese related business is actually pretty strong.

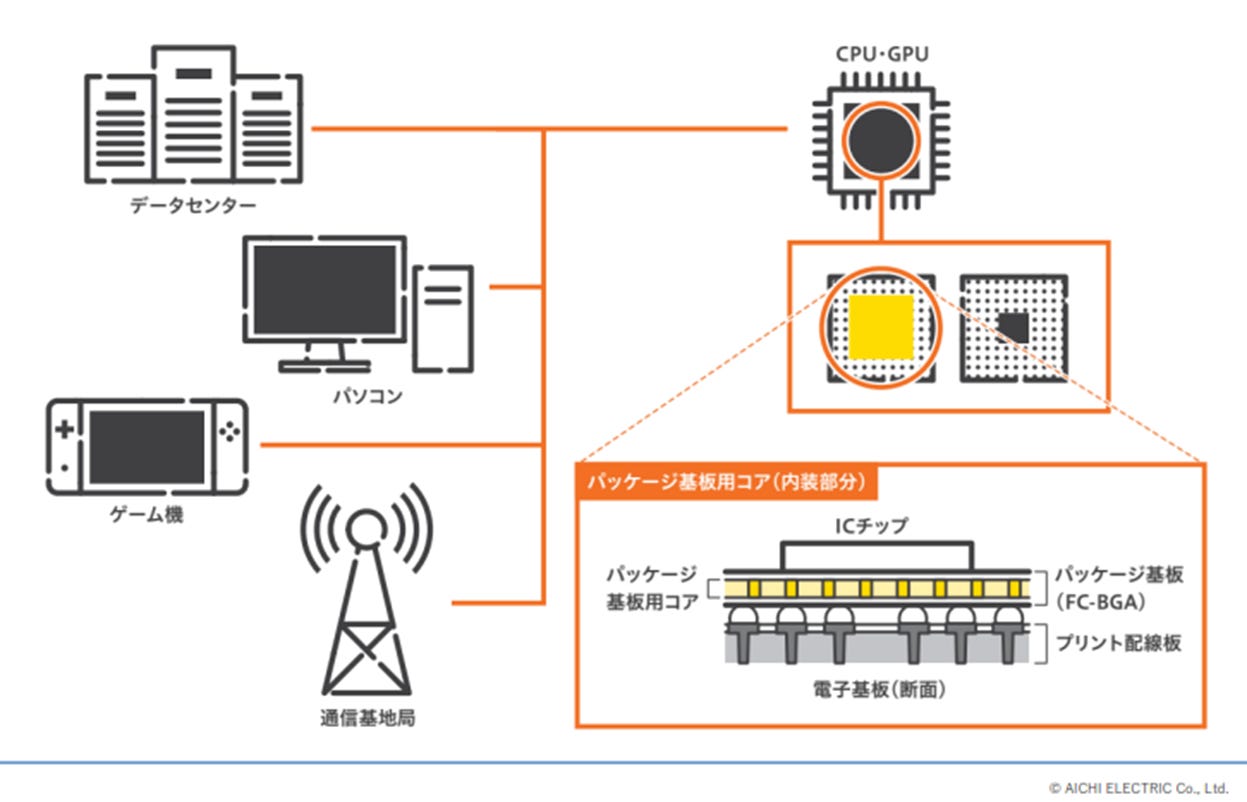

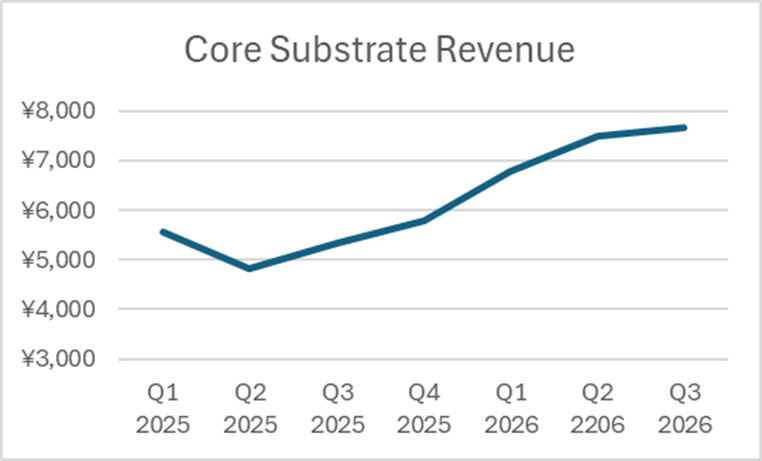

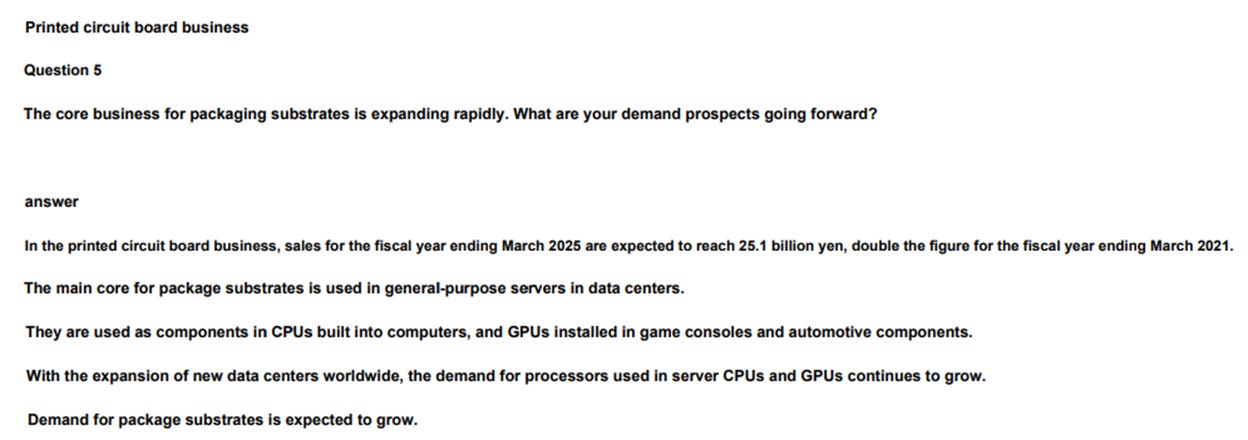

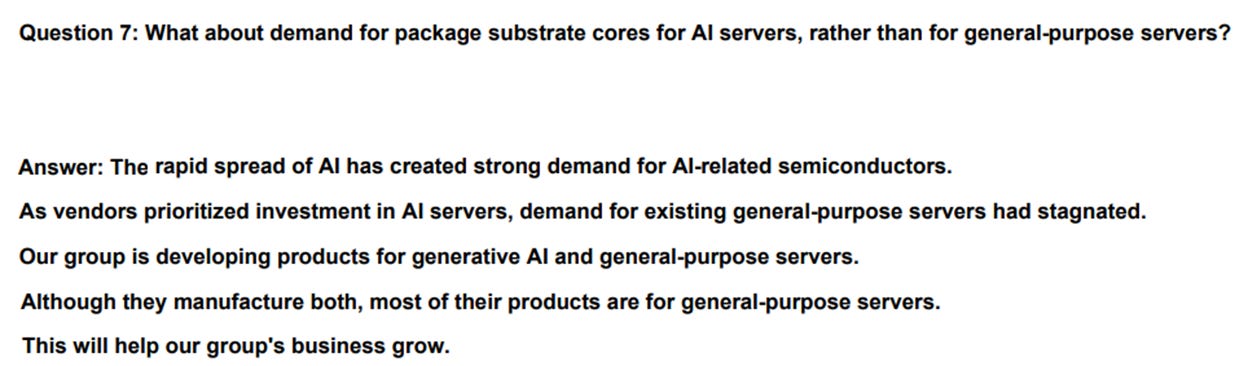

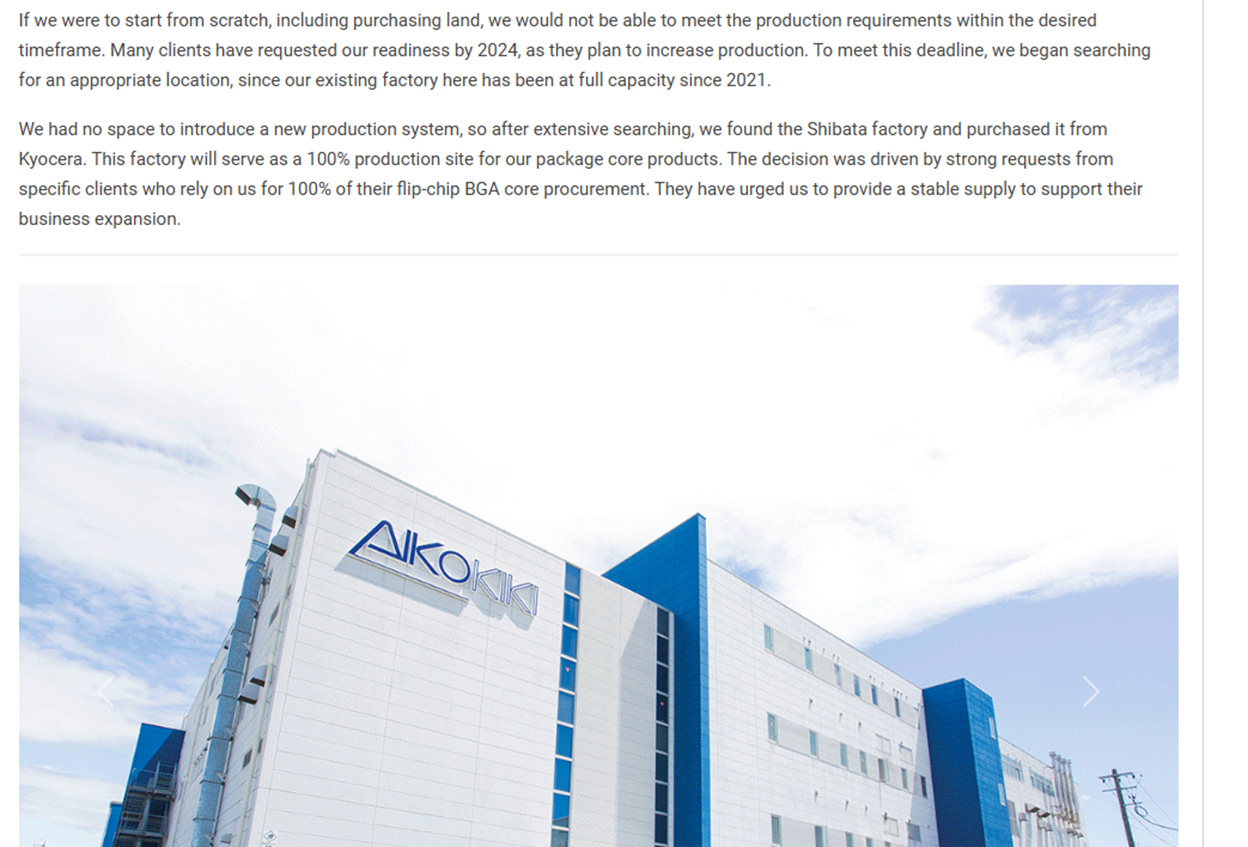

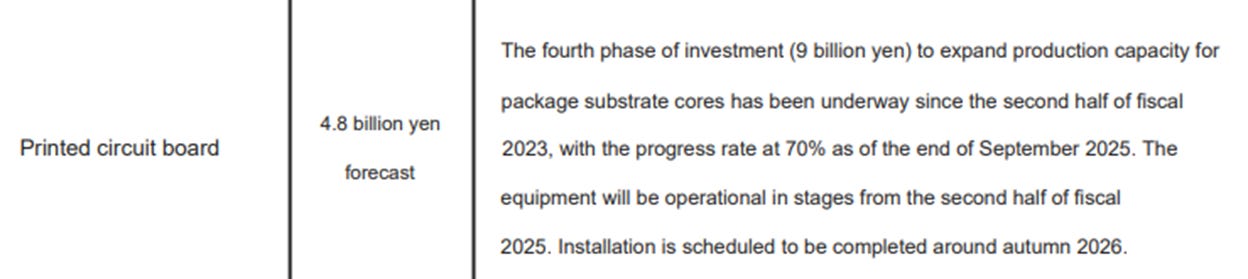

3. Printed Circuit Board (PCB) Division

Now we are getting to the most exciting part of the investment.

The bottom right is a Flip-Chip Ball Grid Array FC-BGA. Aikokiki (Aichi’s subsidiary) specializes in making substrates for semiconductors.

Aikokiki has been aggressively investing in growth in this area in the last few years and results have been very compelling.

https://finance.yahoo.com/news/cpus-are-back-en-vogue-in-the-data-center-184504720.html

CPUs are back en vogue in the data center

“For the last few years, GPUs (graphic processing units) have been the hottest sellers around. Hyperscalers, neoclouds, and everyone in between have been splashing billions to get their hands on the high-end chips to train and run their AI models.

That left the humble CPU (central processing unit), which powers virtually everything else in data centers, and thus the applications and services you use every day, out in the cold.

That’s starting to change, though. Earlier this month, Meta (META) and Nvidia (NVDA) announced an expanded deal that will see Nvidia provide the social media giant with the largest deployment of its Grace CPU-only servers to date.

Then just last week, AMD (AMD) announced its own deal with Meta, which includes servers running the company’s Venice and next-generation Verano CPUs.

And during Intel’s (INTC) Jan. 22 earnings call, CEO Lip-Bu Tan cited AI as a major driver for CPU demand.

“The continuing proliferation and diversification of AI workloads is placing significant capacity constraints on traditional and new hardware infrastructure, reinforcing the growing and essential role CPUs play in the AI era,” Tan said.

It might sound counterintuitive for CPUs to grab some of the spotlight amid the global AI buildout, but in a world where AI inference and agentic AI are becoming increasingly important, CPUs, it turns out, are primed to shine.”

https://pcbmake.com/fc-bga-substrate/

Aikokiki specializes in FC-BGA core substrates that are used in CPUs and gaming GPUs. The company is just completing a large investment to increase capacity and proeduce higher value, multi-layered core substrates.

Remember earlier that PCB division (Aikokiki) has been achieving around 30% after-tax ROE on its investments. On a Y9 billion investment that is around Y3 billion. That would take forward earnings to about Y6.5 billion. At 20% ROE, we get forward earnings of Y5.5 billion.

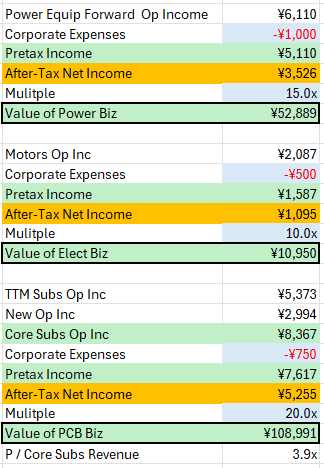

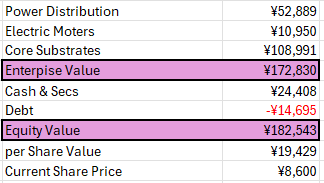

Aichi Electric Valuation

The two other companies that make core substrates are Kinsus in Taiwan and Daeduck in South Korea. Kinsus trades for 3.7x revnue and 84x P/E ratio. Daeduck for 3.2x revenue and 140x P/E ratio.

Thanks for writing this up, Nick. A couple questions:

- you assume 30% ROEs going forward. why in 2021 did ROEs jump 50% from 20% to 30%, and is that truly able to be sustained going forward? the incremental roa suggests they are getting less efficient on assets (capex), not more

- could you elaborate on the ability/inability to pass on prices?

- what sort of contracts are they historically taken with? eg is it locked up? can customers pull orders easily?

- Myles

Thanks for introducing a company I hadn’t looked at before.

That’s an interesting and unusual positioning they have in the packaging supply chain as a supplier of semi-finished cores. Most (all?) organic substrate players are vertically integrated across core and build-up steps, so it seems Aikokiki are supplying such companies as a secondary / transitional supplier to address in-house bottlenecks.